Lithium

Estimates of global lithium uses in 2011

Ceramics and glass (29%)

Batteries (27%)

Lubricating greases (12%)

Continuous casting (5%)

Air treatment (4%)

Polymers (3%)

Primary aluminum production (2%)

Pharmaceuticals (2%)

Other (16%)

Lithium and its compounds have several industrial applications, including heat-resistant glass and ceramics, high strength-to-weight alloys used in aircraft, lithium batteries and lithium-ion batteries. These uses consume more than half of lithium production. In the later years of the 20th century, owing to its high electrochemical potential, lithium became an important component of the electrolyte and of one of the electrodes in batteries. A typical lithium-ion battery can generate approximately 3 volts, compared with 2.1 volts for lead-acid or 1.5 volts for zinc-carbon cells. Because of its low atomic mass, it also has a high charge- and power-to-weight ratio. Lithium batteries are disposable (primary) batteries with lithium or its compounds as an anode. Lithium batteries are not to be confused with lithium-ion batteries, which are high energy-density rechargeable batteries. Other rechargeable batteries include the lithium-ion polymer battery, lithium iron phosphate battery, and the nanowire battery.

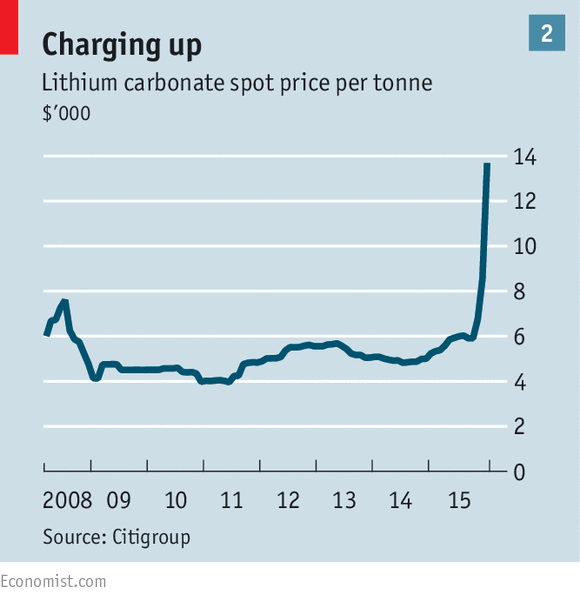

There is no international spot price for lithium. Numerous lithium compounds are sold. The price will depend on the type, purity, particle size, packaging etc. It has been announced that SQM (Chile), the world’s largest supplier of lithium products, will reduce the price of lithium carbonate and lithium hydroxide by 20% at the beginning of 2010. The new prices will be in the range of US$5,000 - 5,400 per tonne (US$2.3-2.4/ per lb). The reason for the decrease in the price is to accelerate the demand recovery and create incentives for researching new uses for lithium (Industrial Minerals, 2009a).

Technical grade carbonate, used for the manufacturing of batteries, cost US$6,613 per tonne in March 2009 (Madison Avenue Research Group, 2009).

The

latest Chile monthly export data shows lithium carbonate prices lower

by 2.3% for the year 2014 at US$4,600 per tonne.

The price of 99%-pure lithium carbonate imported to China more than doubled in the two months to the end of December 2015, to $13,000 a tonne

The price of 99%-pure lithium carbonate imported to China more than doubled in the two months to the end of December 2015, to $13,000 a tonne

Enirgi Group's New Technology Allows Significant Lithium Extraction

Lithium has all the elements of a very sound investment as it powers future

By Jesse Riseborough (The Independent)

Thursday, July 05, 2012

INVESTORS from JPMorgan Chase to BlackRock are trying to make money from the exploding popularity of iPads and increasing sales of hybrid cars by investing in producers of lithium for batteries.

Prices for the conductive metal, the lightest in the periodic table, have tripled since 2000 in a market now worth $1bn (€794m) a year as uses expand in vehicles, ceramics, electronics and lubricants.

Apple and Toyota, maker of the Prius electric-gasoline car, have few alternatives as they pursue higher performance and mobility, leading Dahlman Rose analysts to forecast lithium demand will double by 2020.

Talison Lithium, whose shares have gained 22pc in the last month, together with Soc. Quimica & Minera de Chile SA, Rockwood Holdings and FMC, account for almost 95pc of world supply.

Rio Tinto Group, the third-biggest mining company, may join the largest suppliers if it goes ahead with a mine in Serbia it says is capable of producing 20pc of global output of the metal.

"There are some companies now that we think are attractive to get a hold of lithium exposure," Evy Hambro, who manages about $13bn in mining stocks for BlackRock in London, said. "We've got a small exposure today and we're looking for some more," he added without naming any companies.

Doubled

Demand for lithium-ion rechargeable batteries out of Asia has helped prices climb threefold in the last 12 years, London- based Roskill Information Services analyst Robert Baylis said. Global use doubled from 2000 to 2011, according to Roskill, which has recently consulted on six lithium projects.

The advantage of lithium-ion over other battery types is that a typical cell can generate môre electricity than competing cells such as lead-acid. There is about 1.7 grams of lithium carbonate equivalent in a mobile phone, 2.1 grams in a smartphone and 20 grams in a tablet, according to Dahlman Rose.

There will be a "step change", in the global lithium industry in 2016 or 2017 when electric cars become more commonplace, Rockwood chief executive officer Seifollah Ghasemi said. Hybrid electric vehicles that are fitted with a lithium-ion battery contain about 1.3kg of the material, plug-in hybrid electric vehicles have about 12.8kg, while an electric vehicle uses about 19.2kg.

The four-strong lithium "oligopoly has the capacity to significantly ramp supply higher, but it will take time and significant capital to accomplish," Dahlman Rose analysts Anthony Young and Anthony Rizzuto said in a May 16 report. "There are a limited number of known high-grade resources that can be economically extracted and there has not been a new lithium mine constructed in the last 25 years." Global consumption may jump to 300,000 metric tons a year by 2020 from about 150,000 tons now, Dahlman Rose said in a June report. Demand for lithium batteries has been growing at about 25pc a year, outpacing the 4pc to 5pc overall gain in lithium, the firm said.

"Anywhere between a doubling and a tripling of demand in the next 10 years is absolutely our view," said Peter Oliver, head of Talison, the biggest producer.

"Maybe a doubling is with minimal impact from electric vehicles and if electric vehicles take off in a big way in the next 10 years it could be as much as tripling."

Neil Gregson, manager of about $6.9bn in natural resource assets at JPMorgan Asset Manag"You can't see any reason why that won't be a high growth market for many, many years. It's.a. very interesting area."

Chile, the second-biggest producing country behind Australia, last month said it will award 20-year concessions to exploit lithium brine in salt lakes. The plan allows developers to mine as much as 100,000 metric tons of the mineral over 20 years.

'Critical'

Rio's Jadar project is in pre-feasibility, which involves conducting studies to better understand the parameters of the deposit and any social and environmental impacts, the company said.

Lithium is "going to be so critical to that future world of electric vehicles and hybrids", Tom Albanese, CEO of Rio Tinto, said in London back in April. "We've got a lot of interest from Japanese companies, from Korean companies that actually want to be in the forefront of hybrid and lithium technologies so I'm actually pretty excited about the project." General Motors' Chevrolet Volt was the best-selling rechargeable car in the US in May, topping Toyota's Prius and Nissan Motor's all-electric Leaf hatchback. Deliveries of the GM plug-in sedan more than tripled in the month. Suppliers of lithium have benefited as some car-makers switch from older model nickel-cadmium batteries to lithium-ion.

Rockwood proposed a price increase of $1,000 a tonne in May, or about 22pc, for lithium salt sold to customers in the year starting July 1. It said the higher price would allow it to fund expansion of its mines. Talison's Oliver said he raised prices 15pc in the first-half and expects to increase prices again in the second-half. "The outlook for lithium is very strong in light of some of the uncertainty of other metals such as copper and many of the industrial metals," Jonathan Lee, a battery materials and technologies analyst at Byron Capital Markets, said. "Lithium has grown roughly at 10 to 15pc over the past two years on a per-annum basis. We're having another strong year this year." (Bloomberg)

- Jesse Riseborough

The current global end-use markets for lithium are:

Batteries - 25%

Ceramics and glass - 18%

Lubricating greases - 12%

Pharmaceuticals and polymers - 7%

Air conditioning - 6%

Primary aluminium production - 4%

Continuous casting - 3%

Chemical processing - 3%

Various other uses - 22%

(Madison Avenue Research Group, 2009).

The outlook for lithium consumption is positive. It is reported that lithium demand is expected to increase three fold within ten years as a direct result of increased demand for secondary (rechargeable) batteries and Electric Vehicle (EV) batteries.

Current lithium (Lithium Carbonate Equivalent) global demand is 110,000 tpa. This is expected to rise to 250,000-300,000 tpa by 2020.

SOURCES OF LITHIUM

The principle sources of lithium are brines and to a lesser extent, pegmatites. Lithium is also found in the montmorillonite group clays such as hectorite.

CLAYS

CLAYS

Bulk

sampling of the upper hectorite clays in Western Lithium's Humboldt

county site, Nevada, during the summer of 2013.(Photo:

Provided by Western Lithium)

A

piece of hectorite clay from Western Lithium's exploration site in

Humboldt County, Nevada. The company plans to extract lithium from

the material.(Photo: Provided

by Western Lithium)

BRINES

An

aerial view of the brine pools and processing areas of the Soquimich

lithium mine on the Atacama salt flat, the largest lithium deposit

currently in production, in the Atacama desert of northern Chile, on

Jan. 10, 2013. (Ivan

Alvarado / Reuters)

Lithium compounds are found in continental, geothermal and oilfield brines. The brines are formed by the chemical weathering of lithium-bearing rocks by hydrothermal fluids, particularly in restricted basins, in areas of high evaporation. The brines are generally sourced from the porous strata beneath the surface of the basins. Some of the lithium may be sourced through the leaching of volcanic ash, clays and rocks, however lithium is not easily leached from rock unless exposed to hot fluids in the region of 275- 600°C.

The major producers of lithium from brines are Chile, Argentina, Bolivia, the USA and China.

The lithium content of some of these brines is as follow:

- Salar de Atacama salt flat in Chile; 1570 ppm

- Salar de Surrie in Chile; 389 ppm, 1334 ppm B and 1120 ppm K.

- Olaroz lithium-potash project, Jujuy Province, Argentina; 700 ppm

- Clayton Valley (Silver Peak), Nevada, U S A; During production the grade was 400 ppm, this slowly declined and in 1998 it was 100-300 ppm

- Searles Lake, California, U S A, 50-80 ppm Li, but lithium production has ceased and only soda ash is produced currently.

Alkaline brine dry lake sources in Chile, China and Argentina produce lithium chloride directly. Lithium chloride is converted to lithium carbonate and lithium hydroxide by reaction with sodium carbonate and calcium hydroxide respectively.

PEGMATITES

Year of Estimate: 2009

| Rank | Country | World Production, By Country (Metric tons) in 2009 | |

|---|---|---|---|

| 1 | Australia | 200,000 | |

| 2 | China | 20,000 | |

| 3 | Zimbabwe | 20,000 | |

| 4 | Canada | 10,000 | |

| 5 | Brazil | 8,000 | |

Lithium containing pegmatites are relatively rare and are commonly associated with tin and tantalite. Very large (MgO+FeO)/Li2O ratios exist during the early stages of magma cooling, and the consequent crystallization of ferromagnesian minerals results in the concentration of lithium in the residual magmatic fluids. As pegmatites form by the late crystallization of postmagmatic fluids they are often enriched in lithium. There are numerous pegmatite-hosted lithium-bearing minerals but only five have been commercially exploited:

Source: Wikipedia

Lepidolite (KLi2AlSi4O10(F, OH, O))

Source: www.auburn.edu

Petalite (Li2O.Al2O3.8SiO2)

Source: www.mineralminers.com

GLOBAL RESERVES

The current global resources and reserves of lithium are estimated at 30.12 Mt (160 Mt of lithium carbonate equivalent) (Madison Avenue Research Group, 2009).

Source: U.S. Geological Survey, Mineral Commodity Summaries, February 2014

Identified

lithium resources total 5.5 million tons in the United States and

approximately 34 million tons in other countries. Identified lithium

resources for Bolivia and Chile are 9 million tons and in excess of

7.5 million tons, respectively. Identified lithium resources for

Argentina, China, and Australia are 6.5 million tons,5.4 million

tons, and 1.7 million tons, respectively. Canada, Congo (Kinshasa),

Russia, and Serbia have resources of approximately 1 million tons

each. Identified lithium resources for Brazil total 180,000 tons.

(Source: USGS)

Companies producing and exploring for lithium

- SQM (Sociedad Quimica y Minera de Chile ) based in Chile is the world's largest lithium producer from lithium containing brine from the Salar de Atacama. The company produces lithium carbonate, lithium hydroxide and lithium chloride as by products of specialty plant nutrients and chemicals commodities. SQM is producing lithium carbonate with an installed capacity of 40,000 ton/year and lithium hydroxide with an installed capacity of 6,000 ton/year.

- Albemarle Corporation acquired Rockwood Holdings, Inc. in 2015, in a cash and stock transaction valued at approximately $6.2 billion. The acquisition made Albemarle one of the world's premier specialty chemicals companies, with market-leading positions across four high-margin businesses: lithium, catalysts, bromine and surface treatment. Chemetall SCL (Sociedad Chilena de Litio).SCL, which Rockwood acquired in 2004, is producing lithium carbonate with a capacity of about 22,000 ton/year and lithium chloride with a capacity of about 4,000 ton/year at Salar de Atacama. In the 1960s, Foote pioneered the production of lithium carbonate from brine with the opening of the Silver Peak, NV plant. In 1984, the brine deposit went on stream at Salar de Atacama in the desert of northern Chile. Today, the Silver Peak and Salar de Atacama plants combine to produce in excess of 60,000 tonnes of lithium carbonate equivalents per year.

- FMC Minera del Altiplano is a subsidiary of the FMC Lithium Division involved in lithium mining and processing in Argentina. Its production facilities include Selective Absorption and Lithium Carbonate plants at Salar del Hombre Muerto in the Argentine Andes, and a Lithium Chloride plant in Guemes City, Salta Province. At Minera del Altiplano’s production operations, processing of Lithium Carbonate is based on Lithium Chloride solutions obtained as a by-product of Potassium Chloride. Lithium Chloride solutions are processed to produce Lithium Carbonate. Brines that are not used are re-injected into the salt flats. The Salar del Hombre Muerto is located in the high Andes (13,200 feet above sea level) about 850 miles northwest of Buenos Aires. The location is convenient to major rail lines and seaports. Covering a smaller area than most salars of the region, it contains lithium brines at depths much greater than its neighbors. Lithium reserves are sufficient for well over 75 years.

- Talison Lithium is a leading global producer of lithium. Talison Lithium currently produces lithium concentrate at its lithium mineral project in Western Australia located in the town of Greenbushes. The lithium orebody at Greenbushes is unique in that it contains large zones of high grade lithium ore. Lithium has been produced from the Greenbushes operations for over 25 years and Talison Lithium currently exports over 350,000 tonnes of lithium products annually to a global customer base. Talison Lithium also has a lithium brine project located in the Atacama Region III, in Chile. This prospective exploration project consists of seven salars (brine lakes and surrounding concessions). Five of the salars are clustered within a radius of approximately 30kms and are 100% owned by Talison Lithium and its Chilean partners.

The only source of lithium

in Namibia to date has been pegmatites, where it typically occurs and

was recovered with beryllium, cesium, rare earths and tantalite

(Diehl, 1992).

- Namaqualand Metamorphic Complex

The pegmatites are

intruded into gneisses and ultramafic rocks of Mokolian age in

southern Namibia (Diehl, 1992).

Lepidolite

pegmatite

The pegmatite is

located between the farms Umeis 110 and Kinderzitt 132 about 0.75 km

southwest of the Signaalberg. It has intruded peridotite, pyroxenite

and troctolite of the Tantalite Valley Complex. The body is 200m long

and up to 10m wide. The body is zoned and consists of a border and

wall zone of quartz, perthite, albite and minor muscovite. There are

two intermediate zones that are more differentiated and consist of

massive lepidolite, albite, quartz and accessory minerals including

spodumene, amblygonite, rubellite, tantalite and microlite (Diehl,

1992).

Sandfontein-Ramansdrift Pegmatites

The pegmatites are

located on the farms Sandfontein 131, Sandfontein West 148,

Sperlingsputz 259, Witputz 258, Hochfeld 112 Norechab 129,

Haakiesdoorn 137, Gaobis 138, Gaidip 146 and Ramansdrift 235. The

pegmatites contain niobium-tantalum, lithium, beryllium and rare

earth mineralisation. The pegmatites are intruded into the

metavolcanic rocks of the Huab Formation and the plutonic rocks of

the Vioolsdrif Suite. They range in width from 3 to 30m and are 100

to 250m long. The mineral composition includes quartz, microcline,

microcline-perthite, schorl, biotite, magnetite, sphene, beryl,

tantalite-columbite and microlite (Diehl, 1992).

Karibib-Usakos Pegmatite District

The most significant

pegmatitic lithium deposits within Namibia occur in the

Karibib-Usakos pegmatite district in the Damara Succession (Diehl,

1992). These pegmatites are associated with granites intruded into

the Damara sequence. The area hosts numerous mineralized rare earth

pegmatites which could be an important source of lithium, cesium,

rubidium, beryllium, niobium, tantalum and bismuth. The pegmatite

field is approximately 200km long and 100km wide. It is one of the

most extensive pegmatite fields in the world (Baldwin, 1989). The

pegmatites exhibit a typical geochemical pattern where Li, Na and K

phases are well developed. The common minerals found include

lepidolite, petalite, amblygonite, Li-Mn-Fe phosphates, spodumene,

muscovite, beryl and tourmaline (Balwin,1989 and Diehl, 1992).

- BlackFire Minerals Ltd (Australian) has acquired the exploration rights to the more important defunct lithium workings (Rubikon, Helikon) from Australian private company Sunrise Minerals Pty Ltd. The acquisition was facilitated via Black Fire purchasing Sunrise’s private Namibian subsidiary, Starting Right Investments Ninety Four (Pty) Ltd, which is the holder of Exclusive Prospecting Licences EPL 3750 and EPL 3751.

Rubikon

Pegmatite

The

pegmatite is the largest of the Rubikon pegmatite swarm and is

located 30km southeast of Karibib on the farm Okongava 72.

The pegmatite belongs to the group of internally zoned Li-Cs-Be-Rb

pegmatites. It has reached the highest degree of alkali

fractionation. It has been the major source of lithium within

Namibia. The deposit was exploited by open pit and room-and-pillar

stoping to a depth of 30m (Diehl, 1992).

The pegmatite

consists of two ellipsoidal, well zoned, lithium bearing orebodies

that are surrounded by quartzo-feldspathic pegmatite. It is intruded

into quartz monzodiorite and pegmatitic two-mica granite of Pan

African age (Diehl and Schneider, 1990). The first ore body is 320m

long and 25 to 35m wide and dips 45° to the northeast but flattens

to 18 to 25° at depth. The second ore body dips 30° to the

northeast and flattens to 8 to 12° at a depth of 20m.

Mineralogically

the ore body can be divided from the footwall into the following

zones (Diehl and Schneider, 1990):

Border Zone

Wall Zone

Outer Intermediate Zone

Inner Intermediate Zone

Outer Core Zone

Beryl Zone

Petalite Zone

Low-grade Lepidolite Zone

High-grade Lepidolite Zone

Inner Core Zone

Perthite-Quartz Core

Petalite Zone

Quartz-Core

The exploitable

lithium minerals are confined to the outer and inner core zones.

Economic quantities of beryl are also found in the bodies (Diehl,

1992).

Pinkish petalite crystals in the upper portion of the Rubikon pegmatite,Namibia

Helikon

Pegmatites

The pegmatites are

located 30km southeast of Karibib on the farm Okongava Ost

72. There are two pegmatites, Helikon I and

Helikon II. The pegmatites are rare metal bearing and lithium rich.

They both have been mined for lepidolite, amblygonite, petalite, mica

and by- products that include beryl, pollucite, quartz and

columbite-tantalite (Diehl, 1992).

Dernburg Pegmatite

The pegmatite is

located west-southwest of Karibib on the farm Karibib Townlands

57. The pegmatite intruded into the Chuos Formation quartzites.

The pegmatite strikes west-northwest and dips steeply to the

southwest (Diehl, 1992). It is considered a lithium-beryllium rare

earth metal pegmatite. There are a number of symmetrical zonations

that are discontinuous along strike (Diehl, 1992). The zones are as

follows:

Border zone

(quartz, muscovite, albite)

Wall zone (albite,

quartz, muscovite)

Outer intermediate

zone (perthite, quartz,

muscovite, albite)

Inner intermediate

zone (albite, quartz, muscovite, beryl, amblygonite)

Outer core zone

(spodumene, amblygonite,

cleavelandite,

muscovite)

Inner core zone

(massive quartz)

Amblygonite is

found as nodular crystals within the inner intermediate zone. The

amblygonite is associated with irregularly distributed quartz masses.

Cleavelandite, beryl, topaz and spodumene occur along the margin of

inner core zone (Roering, 1963).

Karlsbrunn

Pegmatite

The pegmatite is

located 6.5km south-southwest of the railway siding at Albrechtshohe.

The pegmatite is 30 to 150m wide and has a strike length of 330m. It

has intruded the Karibib Formation marbles (Diehl, 1992). The

pegmatite exhibits zoning and is divided as follows:

Border zone

Wall zone

Inner intermediate

zone (perthite, quartz, albite-cleavelandite, muscovite, beryl)

Outer core zones

(petalite-amblygonite and lepidolite)

Core margin zone

(albite, beryl, columbite, apatite)

Inner core zone

(massive quartz)

Estimates of global lithium uses in 2011

Ceramics and glass (29%)

Batteries (27%)

Lubricating greases (12%)

Continuous casting (5%)

Air treatment (4%)

Polymers (3%)

Primary aluminum production (2%)

Pharmaceuticals (2%)

Other (16%)

Lithium and its compounds have several industrial applications, including heat-resistant glass and ceramics, high strength-to-weight alloys used in aircraft, lithium batteries and lithium-ion batteries. These uses consume more than half of lithium production. In the later years of the 20th century, owing to its high electrochemical potential, lithium became an important component of the electrolyte and of one of the electrodes in batteries. A typical lithium-ion battery can generate approximately 3 volts, compared with 2.1 volts for lead-acid or 1.5 volts for zinc-carbon cells. Because of its low atomic mass, it also has a high charge- and power-to-weight ratio. Lithium batteries are disposable (primary) batteries with lithium or its compounds as an anode. Lithium batteries are not to be confused with lithium-ion batteries, which are high energy-density rechargeable batteries. Other rechargeable batteries include the lithium-ion polymer battery, lithium iron phosphate battery, and the nanowire battery.

Petalite (Li2O.Al2O3.8SiO2)

Source: www.realmagick.com

Lithium News

PRICES

There is no international spot price for lithium. Numerous lithium compounds are sold. The price will depend on the type, purity, particle size, packaging etc. It has been announced that SQM (Chile), the world’s largest supplier of lithium products, will reduce the price of lithium carbonate and lithium hydroxide by 20% at the beginning of 2010. The new prices will be in the range of US$5,000 - 5,400 per tonne (US$2.3-2.4/ per lb). The reason for the decrease in the price is to accelerate the demand recovery and create incentives for researching new uses for lithium (Industrial Minerals, 2009a).

Technical grade carbonate, used for the manufacturing of batteries, cost US$6,613 per tonne in March 2009 (Madison Avenue Research Group, 2009).

The latest Chile monthly export data shows lithium carbonate prices lower by 2.3% for the year 2014 at US$4,600 per tonne.

The price of 99%-pure lithium carbonate imported to China more than doubled in the two months to the end of December 2015, to $13,000 a tonne

List of tech metals stocks with latest financial data

Enirgi Group's New Technology Allows Significant Lithium Extraction

Lithium has all the elements of a very sound investment as it powers future

By Jesse Riseborough (The Independent)

Thursday, July 05, 2012

INVESTORS from JPMorgan Chase to BlackRock are trying to make money from the exploding popularity of iPads and increasing sales of hybrid cars by investing in producers of lithium for batteries.

Prices for the conductive metal, the lightest in the periodic table, have tripled since 2000 in a market now worth $1bn (€794m) a year as uses expand in vehicles, ceramics, electronics and lubricants.

Apple and Toyota, maker of the Prius electric-gasoline car, have few alternatives as they pursue higher performance and mobility, leading Dahlman Rose analysts to forecast lithium demand will double by 2020.

Talison Lithium, whose shares have gained 22pc in the last month, together with Soc. Quimica & Minera de Chile SA, Rockwood Holdings and FMC, account for almost 95pc of world supply.

Rio Tinto Group, the third-biggest mining company, may join the largest suppliers if it goes ahead with a mine in Serbia it says is capable of producing 20pc of global output of the metal.

"There are some companies now that we think are attractive to get a hold of lithium exposure," Evy Hambro, who manages about $13bn in mining stocks for BlackRock in London, said. "We've got a small exposure today and we're looking for some more," he added without naming any companies.

Doubled

Demand for lithium-ion rechargeable batteries out of Asia has helped prices climb threefold in the last 12 years, London- based Roskill Information Services analyst Robert Baylis said. Global use doubled from 2000 to 2011, according to Roskill, which has recently consulted on six lithium projects.

The advantage of lithium-ion over other battery types is that a typical cell can generate môre electricity than competing cells such as lead-acid. There is about 1.7 grams of lithium carbonate equivalent in a mobile phone, 2.1 grams in a smartphone and 20 grams in a tablet, according to Dahlman Rose.

There will be a "step change", in the global lithium industry in 2016 or 2017 when electric cars become more commonplace, Rockwood chief executive officer Seifollah Ghasemi said. Hybrid electric vehicles that are fitted with a lithium-ion battery contain about 1.3kg of the material, plug-in hybrid electric vehicles have about 12.8kg, while an electric vehicle uses about 19.2kg.

The four-strong lithium "oligopoly has the capacity to significantly ramp supply higher, but it will take time and significant capital to accomplish," Dahlman Rose analysts Anthony Young and Anthony Rizzuto said in a May 16 report. "There are a limited number of known high-grade resources that can be economically extracted and there has not been a new lithium mine constructed in the last 25 years." Global consumption may jump to 300,000 metric tons a year by 2020 from about 150,000 tons now, Dahlman Rose said in a June report. Demand for lithium batteries has been growing at about 25pc a year, outpacing the 4pc to 5pc overall gain in lithium, the firm said.

"Anywhere between a doubling and a tripling of demand in the next 10 years is absolutely our view," said Peter Oliver, head of Talison, the biggest producer.

"Maybe a doubling is with minimal impact from electric vehicles and if electric vehicles take off in a big way in the next 10 years it could be as much as tripling."

Neil Gregson, manager of about $6.9bn in natural resource assets at JPMorgan Asset Manag"You can't see any reason why that won't be a high growth market for many, many years. It's.a. very interesting area."

Chile, the second-biggest producing country behind Australia, last month said it will award 20-year concessions to exploit lithium brine in salt lakes. The plan allows developers to mine as much as 100,000 metric tons of the mineral over 20 years.

'Critical'

Rio's Jadar project is in pre-feasibility, which involves conducting studies to better understand the parameters of the deposit and any social and environmental impacts, the company said.

Lithium is "going to be so critical to that future world of electric vehicles and hybrids", Tom Albanese, CEO of Rio Tinto, said in London back in April. "We've got a lot of interest from Japanese companies, from Korean companies that actually want to be in the forefront of hybrid and lithium technologies so I'm actually pretty excited about the project." General Motors' Chevrolet Volt was the best-selling rechargeable car in the US in May, topping Toyota's Prius and Nissan Motor's all-electric Leaf hatchback. Deliveries of the GM plug-in sedan more than tripled in the month. Suppliers of lithium have benefited as some car-makers switch from older model nickel-cadmium batteries to lithium-ion.

Rockwood proposed a price increase of $1,000 a tonne in May, or about 22pc, for lithium salt sold to customers in the year starting July 1. It said the higher price would allow it to fund expansion of its mines. Talison's Oliver said he raised prices 15pc in the first-half and expects to increase prices again in the second-half. "The outlook for lithium is very strong in light of some of the uncertainty of other metals such as copper and many of the industrial metals," Jonathan Lee, a battery materials and technologies analyst at Byron Capital Markets, said. "Lithium has grown roughly at 10 to 15pc over the past two years on a per-annum basis. We're having another strong year this year." (Bloomberg)

- Jesse Riseborough

MARKETS AND DEMAND

The current global end-use markets for lithium are:

Batteries - 25%

Ceramics and glass - 18%

Lubricating greases - 12%

Pharmaceuticals and polymers - 7%

Air conditioning - 6%

Primary aluminium production - 4%

Continuous casting - 3%

Chemical processing - 3%

Various other uses - 22%

(Madison Avenue Research Group, 2009).

The outlook for lithium consumption is positive. It is reported that lithium demand is expected to increase three fold within ten years as a direct result of increased demand for secondary (rechargeable) batteries and Electric Vehicle (EV) batteries.

Current lithium (Lithium Carbonate Equivalent) global demand is 110,000 tpa. This is expected to rise to 250,000-300,000 tpa by 2020.

SOURCES OF LITHIUM

The principle sources of lithium are brines and to a lesser extent, pegmatites. Lithium is also found in the montmorillonite group clays such as hectorite.

CLAYS

Hectorite sampling for lithium

Bulk sampling of the upper hectorite clays in Western Lithium's Humboldt county site, Nevada, during the summer of 2013.(Photo: Provided by Western Lithium)

Hectorite clay with lithium

A piece of hectorite clay from Western Lithium's exploration site in Humboldt County, Nevada. The company plans to extract lithium from the material.(Photo: Provided by Western Lithium)

BRINES

An aerial view of the brine pools and processing areas of the Soquimich lithium mine on the Atacama salt flat, the largest lithium deposit currently in production, in the Atacama desert of northern Chile, on Jan. 10, 2013. (Ivan Alvarado / Reuters)

Lithium compounds are found in continental, geothermal and oilfield brines. The brines are formed by the chemical weathering of lithium-bearing rocks by hydrothermal fluids, particularly in restricted basins, in areas of high evaporation. The brines are generally sourced from the porous strata beneath the surface of the basins. Some of the lithium may be sourced through the leaching of volcanic ash, clays and rocks, however lithium is not easily leached from rock unless exposed to hot fluids in the region of 275- 600°C.

The major producers of lithium from brines are Chile, Argentina, Bolivia, the USA and China.

The lithium content of some of these brines is as follow:

Salar de Atacama salt flat in Chile; 1570 ppm

Salar de Surrie in Chile; 389 ppm, 1334 ppm B and 1120 ppm K.

Olaroz lithium-potash project, Jujuy Province, Argentina; 700 ppm

Clayton Valley (Silver Peak), Nevada, U S A; During production the grade was 400 ppm, this slowly declined and in 1998 it was 100-300 ppm

Searles Lake, California, U S A, 50-80 ppm Li, but lithium production has ceased and only soda ash is produced currently.

Alkaline brine dry lake sources in Chile, China and Argentina produce lithium chloride directly. Lithium chloride is converted to lithium carbonate and lithium hydroxide by reaction with sodium carbonate and calcium hydroxide respectively.

PEGMATITES

Rank

Country

World Production, By Country (Metric tons) in 2009

1

Australia

200,000

200000

2

China

20,000

20000

3

Zimbabwe

20,000

20000

4

Canada

10,000

10000

5

Brazil

8,000

8000

Source: United States Geological Survey (USGS) Minerals Resources Program

Year of Estimate: 2009

Lithium containing pegmatites are relatively rare and are commonly associated with tin and tantalite. Very large (MgO+FeO)/Li2O ratios exist during the early stages of magma cooling, and the consequent crystallization of ferromagnesian minerals results in the concentration of lithium in the residual magmatic fluids. As pegmatites form by the late crystallization of postmagmatic fluids they are often enriched in lithium. There are numerous pegmatite-hosted lithium-bearing minerals but only five have been commercially exploited:

Spodumene - LiAl(SiO3)2

Source: Wikipedia

Lepidolite (KLi2AlSi4O10(F, OH, O))

Source: www.auburn.edu

Petalite (Li2O.Al2O3.8SiO2)

Source: www.realmagick.com

Amblygonite (2Li(F, OH).Al2O3.P2O5)

Source: www.mineralminers.com

GLOBAL RESERVES

The current global resources and reserves of lithium are estimated at 30.12 Mt (160 Mt of lithium carbonate equivalent) (Madison Avenue Research Group, 2009).

Worldwide Lithium Resources

Source: U.S. Geological Survey, Mineral Commodity Summaries, February 2014

Identified lithium resources total 5.5 million tons in the United States and approximately 34 million tons in other countries. Identified lithium resources for Bolivia and Chile are 9 million tons and in excess of 7.5 million tons, respectively. Identified lithium resources for Argentina, China, and Australia are 6.5 million tons,5.4 million tons, and 1.7 million tons, respectively. Canada, Congo (Kinshasa), Russia, and Serbia have resources of approximately 1 million tons each. Identified lithium resources for Brazil total 180,000 tons. (Source: USGS)

Companies producing and exploring for lithium

SQM (Sociedad Quimica y Minera de Chile ) based in Chile is the world's largest lithium producer from lithium containing brine from the Salar de Atacama. The company produces lithium carbonate, lithium hydroxide and lithium chloride as by products of specialty plant nutrients and chemicals commodities. SQM is producing lithium carbonate with an installed capacity of 40,000 ton/year and lithium hydroxide with an installed capacity of 6,000 ton/year.

Albemarle Corporation acquired Rockwood Holdings, Inc. in 2015, in a cash and stock transaction valued at approximately $6.2 billion. The acquisition made Albemarle one of the world's premier specialty chemicals companies, with market-leading positions across four high-margin businesses: lithium, catalysts, bromine and surface treatment. Chemetall SCL (Sociedad Chilena de Litio).SCL, which Rockwood acquired in 2004, is producing lithium carbonate with a capacity of about 22,000 ton/year and lithium chloride with a capacity of about 4,000 ton/year at Salar de Atacama. In the 1960s, Foote pioneered the production of lithium carbonate from brine with the opening of the Silver Peak, NV plant. In 1984, the brine deposit went on stream at Salar de Atacama in the desert of northern Chile. Today, the Silver Peak and Salar de Atacama plants combine to produce in excess of 60,000 tonnes of lithium carbonate equivalents per year.

FMC Minera del Altiplano is a subsidiary of the FMC Lithium Division involved in lithium mining and processing in Argentina. Its production facilities include Selective Absorption and Lithium Carbonate plants at Salar del Hombre Muerto in the Argentine Andes, and a Lithium Chloride plant in Guemes City, Salta Province. At Minera del Altiplano’s production operations, processing of Lithium Carbonate is based on Lithium Chloride solutions obtained as a by-product of Potassium Chloride. Lithium Chloride solutions are processed to produce Lithium Carbonate. Brines that are not used are re-injected into the salt flats. The Salar del Hombre Muerto is located in the high Andes (13,200 feet above sea level) about 850 miles northwest of Buenos Aires. The location is convenient to major rail lines and seaports. Covering a smaller area than most salars of the region, it contains lithium brines at depths much greater than its neighbors. Lithium reserves are sufficient for well over 75 years.

Talison Lithium is a leading global producer of lithium. Talison Lithium currently produces lithium concentrate at its lithium mineral project in Western Australia located in the town of Greenbushes. The lithium orebody at Greenbushes is unique in that it contains large zones of high grade lithium ore. Lithium has been produced from the Greenbushes operations for over 25 years and Talison Lithium currently exports over 350,000 tonnes of lithium products annually to a global customer base. Talison Lithium also has a lithium brine project located in the Atacama Region III, in Chile. This prospective exploration project consists of seven salars (brine lakes and surrounding concessions). Five of the salars are clustered within a radius of approximately 30kms and are 100% owned by Talison Lithium and its Chilean partners.

Namibia

The only source of lithium in Namibia to date has been pegmatites, where it typically occurs and was recovered with beryllium, cesium, rare earths and tantalite (Diehl, 1992).

Namaqualand Metamorphic Complex

The pegmatites are intruded into gneisses and ultramafic rocks of Mokolian age in southern Namibia (Diehl, 1992).

Lepidolite pegmatite

The pegmatite is located between the farms Umeis 110 and Kinderzitt 132 about 0.75 km southwest of the Signaalberg. It has intruded peridotite, pyroxenite and troctolite of the Tantalite Valley Complex. The body is 200m long and up to 10m wide. The body is zoned and consists of a border and wall zone of quartz, perthite, albite and minor muscovite. There are two intermediate zones that are more differentiated and consist of massive lepidolite, albite, quartz and accessory minerals including spodumene, amblygonite, rubellite, tantalite and microlite (Diehl, 1992).

Sandfontein-Ramansdrift Pegmatites

The pegmatites are located on the farms Sandfontein 131, Sandfontein West 148, Sperlingsputz 259, Witputz 258, Hochfeld 112 Norechab 129, Haakiesdoorn 137, Gaobis 138, Gaidip 146 and Ramansdrift 235. The pegmatites contain niobium-tantalum, lithium, beryllium and rare earth mineralisation. The pegmatites are intruded into the metavolcanic rocks of the Huab Formation and the plutonic rocks of the Vioolsdrif Suite. They range in width from 3 to 30m and are 100 to 250m long. The mineral composition includes quartz, microcline, microcline-perthite, schorl, biotite, magnetite, sphene, beryl, tantalite-columbite and microlite (Diehl, 1992).

Karibib-Usakos Pegmatite District

The most significant pegmatitic lithium deposits within Namibia occur in the Karibib-Usakos pegmatite district in the Damara Succession (Diehl, 1992). These pegmatites are associated with granites intruded into the Damara sequence. The area hosts numerous mineralized rare earth pegmatites which could be an important source of lithium, cesium, rubidium, beryllium, niobium, tantalum and bismuth. The pegmatite field is approximately 200km long and 100km wide. It is one of the most extensive pegmatite fields in the world (Baldwin, 1989). The pegmatites exhibit a typical geochemical pattern where Li, Na and K phases are well developed. The common minerals found include lepidolite, petalite, amblygonite, Li-Mn-Fe phosphates, spodumene, muscovite, beryl and tourmaline (Balwin,1989 and Diehl, 1992).

BlackFire Minerals Ltd (Australian) has acquired the exploration rights to the more important defunct lithium workings (Rubikon, Helikon) from Australian private company Sunrise Minerals Pty Ltd. The acquisition was facilitated via Black Fire purchasing Sunrise’s private Namibian subsidiary, Starting Right Investments Ninety Four (Pty) Ltd, which is the holder of Exclusive Prospecting Licences EPL 3750 and EPL 3751.

Rubikon Pegmatite

The pegmatite is the largest of the Rubikon pegmatite swarm and is located 30km southeast of Karibib on the farm Okongava 72. The pegmatite belongs to the group of internally zoned Li-Cs-Be-Rb pegmatites. It has reached the highest degree of alkali fractionation. It has been the major source of lithium within Namibia. The deposit was exploited by open pit and room-and-pillar stoping to a depth of 30m (Diehl, 1992).

The pegmatite consists of two ellipsoidal, well zoned, lithium bearing orebodies that are surrounded by quartzo-feldspathic pegmatite. It is intruded into quartz monzodiorite and pegmatitic two-mica granite of Pan African age (Diehl and Schneider, 1990). The first ore body is 320m long and 25 to 35m wide and dips 45° to the northeast but flattens to 18 to 25° at depth. The second ore body dips 30° to the northeast and flattens to 8 to 12° at a depth of 20m.

Mineralogically the ore body can be divided from the footwall into the following zones (Diehl and Schneider, 1990):

Border Zone

Wall Zone

Outer Intermediate Zone

Inner Intermediate Zone

Outer Core Zone

Beryl Zone

Petalite Zone

Estimates of global lithium uses in 2011

Ceramics and glass (29%)

Batteries (27%)

Lubricating greases (12%)

Continuous casting (5%)

Air treatment (4%)

Polymers (3%)

Primary aluminum production (2%)

Pharmaceuticals (2%)

Other (16%)

Lithium and its compounds have several industrial applications, including heat-resistant glass and ceramics, high strength-to-weight alloys used in aircraft, lithium batteries and lithium-ion batteries. These uses consume more than half of lithium production. In the later years of the 20th century, owing to its high electrochemical potential, lithium became an important component of the electrolyte and of one of the electrodes in batteries. A typical lithium-ion battery can generate approximately 3 volts, compared with 2.1 volts for lead-acid or 1.5 volts for zinc-carbon cells. Because of its low atomic mass, it also has a high charge- and power-to-weight ratio. Lithium batteries are disposable (primary) batteries with lithium or its compounds as an anode. Lithium batteries are not to be confused with lithium-ion batteries, which are high energy-density rechargeable batteries. Other rechargeable batteries include the lithium-ion polymer battery, lithium iron phosphate battery, and the nanowire battery.

Petalite (Li2O.Al2O3.8SiO2)

Source: www.realmagick.com

Lithium News

PRICES

There is no international spot price for lithium. Numerous lithium compounds are sold. The price will depend on the type, purity, particle size, packaging etc. It has been announced that SQM (Chile), the world’s largest supplier of lithium products, will reduce the price of lithium carbonate and lithium hydroxide by 20% at the beginning of 2010. The new prices will be in the range of US$5,000 - 5,400 per tonne (US$2.3-2.4/ per lb). The reason for the decrease in the price is to accelerate the demand recovery and create incentives for researching new uses for lithium (Industrial Minerals, 2009a).

Technical grade carbonate, used for the manufacturing of batteries, cost US$6,613 per tonne in March 2009 (Madison Avenue Research Group, 2009).

The latest Chile monthly export data shows lithium carbonate prices lower by 2.3% for the year 2014 at US$4,600 per tonne.

The price of 99%-pure lithium carbonate imported to China more than doubled in the two months to the end of December 2015, to $13,000 a tonne

List of tech metals stocks with latest financial data

Enirgi Group's New Technology Allows Significant Lithium Extraction

Lithium has all the elements of a very sound investment as it powers future

By Jesse Riseborough (The Independent)

Thursday, July 05, 2012

INVESTORS from JPMorgan Chase to BlackRock are trying to make money from the exploding popularity of iPads and increasing sales of hybrid cars by investing in producers of lithium for batteries.

Prices for the conductive metal, the lightest in the periodic table, have tripled since 2000 in a market now worth $1bn (€794m) a year as uses expand in vehicles, ceramics, electronics and lubricants.

Apple and Toyota, maker of the Prius electric-gasoline car, have few alternatives as they pursue higher performance and mobility, leading Dahlman Rose analysts to forecast lithium demand will double by 2020.

Talison Lithium, whose shares have gained 22pc in the last month, together with Soc. Quimica & Minera de Chile SA, Rockwood Holdings and FMC, account for almost 95pc of world supply.

Rio Tinto Group, the third-biggest mining company, may join the largest suppliers if it goes ahead with a mine in Serbia it says is capable of producing 20pc of global output of the metal.

"There are some companies now that we think are attractive to get a hold of lithium exposure," Evy Hambro, who manages about $13bn in mining stocks for BlackRock in London, said. "We've got a small exposure today and we're looking for some more," he added without naming any companies.

Doubled

Demand for lithium-ion rechargeable batteries out of Asia has helped prices climb threefold in the last 12 years, London- based Roskill Information Services analyst Robert Baylis said. Global use doubled from 2000 to 2011, according to Roskill, which has recently consulted on six lithium projects.

The advantage of lithium-ion over other battery types is that a typical cell can generate môre electricity than competing cells such as lead-acid. There is about 1.7 grams of lithium carbonate equivalent in a mobile phone, 2.1 grams in a smartphone and 20 grams in a tablet, according to Dahlman Rose.

There will be a "step change", in the global lithium industry in 2016 or 2017 when electric cars become more commonplace, Rockwood chief executive officer Seifollah Ghasemi said. Hybrid electric vehicles that are fitted with a lithium-ion battery contain about 1.3kg of the material, plug-in hybrid electric vehicles have about 12.8kg, while an electric vehicle uses about 19.2kg.

The four-strong lithium "oligopoly has the capacity to significantly ramp supply higher, but it will take time and significant capital to accomplish," Dahlman Rose analysts Anthony Young and Anthony Rizzuto said in a May 16 report. "There are a limited number of known high-grade resources that can be economically extracted and there has not been a new lithium mine constructed in the last 25 years." Global consumption may jump to 300,000 metric tons a year by 2020 from about 150,000 tons now, Dahlman Rose said in a June report. Demand for lithium batteries has been growing at about 25pc a year, outpacing the 4pc to 5pc overall gain in lithium, the firm said.

"Anywhere between a doubling and a tripling of demand in the next 10 years is absolutely our view," said Peter Oliver, head of Talison, the biggest producer.

"Maybe a doubling is with minimal impact from electric vehicles and if electric vehicles take off in a big way in the next 10 years it could be as much as tripling."

Neil Gregson, manager of about $6.9bn in natural resource assets at JPMorgan Asset Manag"You can't see any reason why that won't be a high growth market for many, many years. It's.a. very interesting area."

Chile, the second-biggest producing country behind Australia, last month said it will award 20-year concessions to exploit lithium brine in salt lakes. The plan allows developers to mine as much as 100,000 metric tons of the mineral over 20 years.

'Critical'

Rio's Jadar project is in pre-feasibility, which involves conducting studies to better understand the parameters of the deposit and any social and environmental impacts, the company said.

Lithium is "going to be so critical to that future world of electric vehicles and hybrids", Tom Albanese, CEO of Rio Tinto, said in London back in April. "We've got a lot of interest from Japanese companies, from Korean companies that actually want to be in the forefront of hybrid and lithium technologies so I'm actually pretty excited about the project." General Motors' Chevrolet Volt was the best-selling rechargeable car in the US in May, topping Toyota's Prius and Nissan Motor's all-electric Leaf hatchback. Deliveries of the GM plug-in sedan more than tripled in the month. Suppliers of lithium have benefited as some car-makers switch from older model nickel-cadmium batteries to lithium-ion.

Rockwood proposed a price increase of $1,000 a tonne in May, or about 22pc, for lithium salt sold to customers in the year starting July 1. It said the higher price would allow it to fund expansion of its mines. Talison's Oliver said he raised prices 15pc in the first-half and expects to increase prices again in the second-half. "The outlook for lithium is very strong in light of some of the uncertainty of other metals such as copper and many of the industrial metals," Jonathan Lee, a battery materials and technologies analyst at Byron Capital Markets, said. "Lithium has grown roughly at 10 to 15pc over the past two years on a per-annum basis. We're having another strong year this year." (Bloomberg)

- Jesse Riseborough

MARKETS AND DEMAND

The current global end-use markets for lithium are:

Batteries - 25%

Ceramics and glass - 18%

Lubricating greases - 12%

Pharmaceuticals and polymers - 7%

Air conditioning - 6%

Primary aluminium production - 4%

Continuous casting - 3%

Chemical processing - 3%

Various other uses - 22%

(Madison Avenue Research Group, 2009).

The outlook for lithium consumption is positive. It is reported that lithium demand is expected to increase three fold within ten years as a direct result of increased demand for secondary (rechargeable) batteries and Electric Vehicle (EV) batteries.

Current lithium (Lithium Carbonate Equivalent) global demand is 110,000 tpa. This is expected to rise to 250,000-300,000 tpa by 2020.

SOURCES OF LITHIUM

The principle sources of lithium are brines and to a lesser extent, pegmatites. Lithium is also found in the montmorillonite group clays such as hectorite.

CLAYS

Hectorite sampling for lithium

Bulk sampling of the upper hectorite clays in Western Lithium's Humboldt county site, Nevada, during the summer of 2013.(Photo: Provided by Western Lithium)

Hectorite clay with lithium

A piece of hectorite clay from Western Lithium's exploration site in Humboldt County, Nevada. The company plans to extract lithium from the material.(Photo: Provided by Western Lithium)

BRINES

An aerial view of the brine pools and processing areas of the Soquimich lithium mine on the Atacama salt flat, the largest lithium deposit currently in production, in the Atacama desert of northern Chile, on Jan. 10, 2013. (Ivan Alvarado / Reuters)

Lithium compounds are found in continental, geothermal and oilfield brines. The brines are formed by the chemical weathering of lithium-bearing rocks by hydrothermal fluids, particularly in restricted basins, in areas of high evaporation. The brines are generally sourced from the porous strata beneath the surface of the basins. Some of the lithium may be sourced through the leaching of volcanic ash, clays and rocks, however lithium is not easily leached from rock unless exposed to hot fluids in the region of 275- 600°C.

The major producers of lithium from brines are Chile, Argentina, Bolivia, the USA and China.

The lithium content of some of these brines is as follow:

Salar de Atacama salt flat in Chile; 1570 ppm

Salar de Surrie in Chile; 389 ppm, 1334 ppm B and 1120 ppm K.

Olaroz lithium-potash project, Jujuy Province, Argentina; 700 ppm

Clayton Valley (Silver Peak), Nevada, U S A; During production the grade was 400 ppm, this slowly declined and in 1998 it was 100-300 ppm

Searles Lake, California, U S A, 50-80 ppm Li, but lithium production has ceased and only soda ash is produced currently.

Alkaline brine dry lake sources in Chile, China and Argentina produce lithium chloride directly. Lithium chloride is converted to lithium carbonate and lithium hydroxide by reaction with sodium carbonate and calcium hydroxide respectively.

PEGMATITES

Rank

Country

World Production, By Country (Metric tons) in 2009

1

Australia

200,000

200000

2

China

20,000

20000

3

Zimbabwe

20,000

20000

4

Canada

10,000

10000

5

Brazil

8,000

8000

Source: United States Geological Survey (USGS) Minerals Resources Program

Year of Estimate: 2009

Lithium containing pegmatites are relatively rare and are commonly associated with tin and tantalite. Very large (MgO+FeO)/Li2O ratios exist during the early stages of magma cooling, and the consequent crystallization of ferromagnesian minerals results in the concentration of lithium in the residual magmatic fluids. As pegmatites form by the late crystallization of postmagmatic fluids they are often enriched in lithium. There are numerous pegmatite-hosted lithium-bearing minerals but only five have been commercially exploited:

Spodumene - LiAl(SiO3)2

Source: Wikipedia

Lepidolite (KLi2AlSi4O10(F, OH, O))

Source: www.auburn.edu

Petalite (Li2O.Al2O3.8SiO2)

Source: www.realmagick.com

Amblygonite (2Li(F, OH).Al2O3.P2O5)

Source: www.mineralminers.com

GLOBAL RESERVES

The current global resources and reserves of lithium are estimated at 30.12 Mt (160 Mt of lithium carbonate equivalent) (Madison Avenue Research Group, 2009).

Worldwide Lithium Resources

Source: U.S. Geological Survey, Mineral Commodity Summaries, February 2014

Identified lithium resources total 5.5 million tons in the United States and approximately 34 million tons in other countries. Identified lithium resources for Bolivia and Chile are 9 million tons and in excess of 7.5 million tons, respectively. Identified lithium resources for Argentina, China, and Australia are 6.5 million tons,5.4 million tons, and 1.7 million tons, respectively. Canada, Congo (Kinshasa), Russia, and Serbia have resources of approximately 1 million tons each. Identified lithium resources for Brazil total 180,000 tons. (Source: USGS)

Companies producing and exploring for lithium

SQM (Sociedad Quimica y Minera de Chile ) based in Chile is the world's largest lithium producer from lithium containing brine from the Salar de Atacama. The company produces lithium carbonate, lithium hydroxide and lithium chloride as by products of specialty plant nutrients and chemicals commodities. SQM is producing lithium carbonate with an installed capacity of 40,000 ton/year and lithium hydroxide with an installed capacity of 6,000 ton/year.

Albemarle Corporation acquired Rockwood Holdings, Inc. in 2015, in a cash and stock transaction valued at approximately $6.2 billion. The acquisition made Albemarle one of the world's premier specialty chemicals companies, with market-leading positions across four high-margin businesses: lithium, catalysts, bromine and surface treatment. Chemetall SCL (Sociedad Chilena de Litio).SCL, which Rockwood acquired in 2004, is producing lithium carbonate with a capacity of about 22,000 ton/year and lithium chloride with a capacity of about 4,000 ton/year at Salar de Atacama. In the 1960s, Foote pioneered the production of lithium carbonate from brine with the opening of the Silver Peak, NV plant. In 1984, the brine deposit went on stream at Salar de Atacama in the desert of northern Chile. Today, the Silver Peak and Salar de Atacama plants combine to produce in excess of 60,000 tonnes of lithium carbonate equivalents per year.

FMC Minera del Altiplano is a subsidiary of the FMC Lithium Division involved in lithium mining and processing in Argentina. Its production facilities include Selective Absorption and Lithium Carbonate plants at Salar del Hombre Muerto in the Argentine Andes, and a Lithium Chloride plant in Guemes City, Salta Province. At Minera del Altiplano’s production operations, processing of Lithium Carbonate is based on Lithium Chloride solutions obtained as a by-product of Potassium Chloride. Lithium Chloride solutions are processed to produce Lithium Carbonate. Brines that are not used are re-injected into the salt flats. The Salar del Hombre Muerto is located in the high Andes (13,200 feet above sea level) about 850 miles northwest of Buenos Aires. The location is convenient to major rail lines and seaports. Covering a smaller area than most salars of the region, it contains lithium brines at depths much greater than its neighbors. Lithium reserves are sufficient for well over 75 years.

Talison Lithium is a leading global producer of lithium. Talison Lithium currently produces lithium concentrate at its lithium mineral project in Western Australia located in the town of Greenbushes. The lithium orebody at Greenbushes is unique in that it contains large zones of high grade lithium ore. Lithium has been produced from the Greenbushes operations for over 25 years and Talison Lithium currently exports over 350,000 tonnes of lithium products annually to a global customer base. Talison Lithium also has a lithium brine project located in the Atacama Region III, in Chile. This prospective exploration project consists of seven salars (brine lakes and surrounding concessions). Five of the salars are clustered within a radius of approximately 30kms and are 100% owned by Talison Lithium and its Chilean partners.

Namibia

The only source of lithium in Namibia to date has been pegmatites, where it typically occurs and was recovered with beryllium, cesium, rare earths and tantalite (Diehl, 1992).

Namaqualand Metamorphic Complex

The pegmatites are intruded into gneisses and ultramafic rocks of Mokolian age in southern Namibia (Diehl, 1992).

Lepidolite pegmatite

The pegmatite is located between the farms Umeis 110 and Kinderzitt 132 about 0.75 km southwest of the Signaalberg. It has intruded peridotite, pyroxenite and troctolite of the Tantalite Valley Complex. The body is 200m long and up to 10m wide. The body is zoned and consists of a border and wall zone of quartz, perthite, albite and minor muscovite. There are two intermediate zones that are more differentiated and consist of massive lepidolite, albite, quartz and accessory minerals including spodumene, amblygonite, rubellite, tantalite and microlite (Diehl, 1992).

Sandfontein-Ramansdrift Pegmatites

The pegmatites are located on the farms Sandfontein 131, Sandfontein West 148, Sperlingsputz 259, Witputz 258, Hochfeld 112 Norechab 129, Haakiesdoorn 137, Gaobis 138, Gaidip 146 and Ramansdrift 235. The pegmatites contain niobium-tantalum, lithium, beryllium and rare earth mineralisation. The pegmatites are intruded into the metavolcanic rocks of the Huab Formation and the plutonic rocks of the Vioolsdrif Suite. They range in width from 3 to 30m and are 100 to 250m long. The mineral composition includes quartz, microcline, microcline-perthite, schorl, biotite, magnetite, sphene, beryl, tantalite-columbite and microlite (Diehl, 1992).

Karibib-Usakos Pegmatite District

The most significant pegmatitic lithium deposits within Namibia occur in the Karibib-Usakos pegmatite district in the Damara Succession (Diehl, 1992). These pegmatites are associated with granites intruded into the Damara sequence. The area hosts numerous mineralized rare earth pegmatites which could be an important source of lithium, cesium, rubidium, beryllium, niobium, tantalum and bismuth. The pegmatite field is approximately 200km long and 100km wide. It is one of the most extensive pegmatite fields in the world (Baldwin, 1989). The pegmatites exhibit a typical geochemical pattern where Li, Na and K phases are well developed. The common minerals found include lepidolite, petalite, amblygonite, Li-Mn-Fe phosphates, spodumene, muscovite, beryl and tourmaline (Balwin,1989 and Diehl, 1992).

BlackFire Minerals Ltd (Australian) has acquired the exploration rights to the more important defunct lithium workings (Rubikon, Helikon) from Australian private company Sunrise Minerals Pty Ltd. The acquisition was facilitated via Black Fire purchasing Sunrise’s private Namibian subsidiary, Starting Right Investments Ninety Four (Pty) Ltd, which is the holder of Exclusive Prospecting Licences EPL 3750 and EPL 3751.

Rubikon Pegmatite

The pegmatite is the largest of the Rubikon pegmatite swarm and is located 30km southeast of Karibib on the farm Okongava 72. The pegmatite belongs to the group of internally zoned Li-Cs-Be-Rb pegmatites. It has reached the highest degree of alkali fractionation. It has been the major source of lithium within Namibia. The deposit was exploited by open pit and room-and-pillar stoping to a depth of 30m (Diehl, 1992).

The pegmatite consists of two ellipsoidal, well zoned, lithium bearing orebodies that are surrounded by quartzo-feldspathic pegmatite. It is intruded into quartz monzodiorite and pegmatitic two-mica granite of Pan African age (Diehl and Schneider, 1990). The first ore body is 320m long and 25 to 35m wide and dips 45° to the northeast but flattens to 18 to 25° at depth. The second ore body dips 30° to the northeast and flattens to 8 to 12° at a depth of 20m.

Mineralogically the ore body can be divided from the footwall into the following zones (Diehl and Schneider, 1990):

Border Zone

Wall Zone

Outer Intermediate Zone

Inner Intermediate Zone

Outer Core Zone

Beryl Zone

Petalite Zone

Low-grade Lepidolite Zone

High-grade Lepidolite Zone

Inner Core Zone

Perthite-Quartz Core

Petalite Zone

Quartz-Core

The exploitable lithium minerals are confined to the outer and inner core zones. Economic quantities of beryl are also found in the bodies (Diehl, 1992).

Pinkish petalite crystals in the upper portion of the Rubikon pegmatite,Namibia

Source: http://giantcrystals.strahlen.org/africa/rubicon.htm

Helikon Pegmatites

The pegmatites are located 30km southeast of Karibib on the farm Okongava Ost 72. There are two pegmatites, Helikon I and Helikon II. The pegmatites are rare metal bearing and lithium rich. They both have been mined for lepidolite, amblygonite, petalite, mica and by- products that include beryl, pollucite, quartz and columbite-tantalite (Diehl, 1992).

Dernburg Pegmatite

The pegmatite is located west-southwest of Karibib on the farm Karibib Townlands 57. The pegmatite intruded into the Chuos Formation quartzites. The pegmatite strikes west-northwest and dips steeply to the southwest (Diehl, 1992). It is considered a lithium-beryllium rare earth metal pegmatite. There are a number of symmetrical zonations that are discontinuous along strike (Diehl, 1992). The zones are as follows:

Border zone (quartz, muscovite, albite)

Wall zone (albite, quartz, muscovite)

Outer intermediate zone (perthite, quartz,

muscovite, albite)

Inner intermediate zone (albite, quartz, muscovite, beryl, amblygonite)

Outer core zone (spodumene, amblygonite,

cleavelandite, muscovite)

Inner core zone (massive quartz)

Amblygonite is found as nodular crystals within the inner intermediate zone. The amblygonite is associated with irregularly distributed quartz masses. Cleavelandite, beryl, topaz and spodumene occur along the margin of inner core zone (Roering, 1963).

Karlsbrunn Pegmatite

The pegmatite is located 6.5km south-southwest of the railway siding at Albrechtshohe. The pegmatite is 30 to 150m wide and has a strike length of 330m. It has intruded the Karibib Formation marbles (Diehl, 1992). The pegmatite exhibits zoning and is divided as follows:

Border zone

Wall zone

Inner intermediate zone (perthite, quartz, albite-cleavelandite, muscovite, beryl)

Outer core zones (petalite-amblygonite and lepidolite)

Core margin zone (albite, beryl, columbite, apatite)

Inner core zone (massive quartz)

Albrechtshohe (Brockmann) Pegmatite

The pegmatite is located in the Albrechtshohe-Kaliombo area, 5km southeast of the Albrechts siding. The pegmatite is lense-shaped with an east-west strike. It is 255m long and dips steeply to the north (Diehl, 1992). According to Roering (1963) the pegmatite is divided into the following zones:

Border zone (weathered material)

Wall zone (albite-quartz-muscovite-tourmaline)

Outer intermediate zone (albite-quartzmuscovite, spodumene)

Inner intermediate (economic) zones

Lepidolite-albite zone

Lepidolite-albite-alkali-feldspar zone

Amblygonite-rich zone

Quartz core zone

Berger Pegmatite

The pegmatite is located 6.5km south-southeast of the Albrechshohe siding on the farm Kaliombo 119. The pegmatite is described as a steeply dipping, east-west striking dyke. It is 160m long. The pegmatite has intruded the Karibib Formation marbles (Diehl, 1992). The pegmatite was divided into the following zones (Roering, 1963):

Border zone (albite-quartz-tourmaline)

Wall zone (albite-quartz-muscovite)

Outer intermediate zone (complex albite-quartz-muscovite)

Inner intermediate zone

Beryl zone

Lepidolite zone

Clay mineral zone

Core zone (quartz)

Euhedral aquamarine and beryl are associated with the outer intermediate zone. The main beryl mineralisation is confined to the inner intermediate zone (Roering, 1963).

Kaliombo Pegmatite (Berger’s Claims)

The pegmatite is located 1.8km south of the Berger pegmatite and is found on the farm Kaliombo 119. The pegmatite has previously been worked. Columbite-tantalite, lepidolite, amblygonite and beryl have been extracted from small lenses within the zoned rare metal pegmatite, which occurs in pegmatitic granite. The lenses are irregularly distributed and vary in compostion from albite- quartz rocks with lepidolite to quartz-rich albite-amblygonite pegmatite. The mineralisation is generally concentrated in the discontinuous quartz core which is partially replaced by cleavelandite- lepidolite- amblygonite assemblages (Diehl, 1992).

Gamikaubmund (Brockmann’s claims)

The pegmatite is located 8km southeast of the Swakop River on the farm Tsaobismund 85. It has intruded the Lower Nossob quartzites. The pegmatite has been exploited for beryl, lithium minerals and columbite-tantalite (Smith, 1965).

Otjua (Becker’s) Pegmatite

The pegmatite is located 33.5km east- southeast of Karibib on the farm Otjua 37. It has been exploited for tourmaline, lepidolite, amblygonite, beryl and smoky quartz. The inner intermediate zone was exploited (Diehl, 1992).

Ricksburg Pegmatite

The pegmatite is located on the farm Okakoara 43. It is a columbite-tantalite lithium-bearing pegmatite (Diehl, 1992). No further information is available

Mon Repos Pegmatite

The pegmatite is located on the farm Navachab 58. Lithium and tantalite minerals were found in this zoned rare metal pegmatite (Diehl, 1992).

Okatjimukuju (Meyer’s Camp, Frickers’s) Pegmatite

The pegmatite is located on the farm Okatjimukuju 55. It is a zoned rare metal pegmatite containing lepidolite and amblygonite. The lithium mineralisation is associated with a muscovite-cleavelandite unit found along the margin of the quartz core (Diehl, 1992).

Etusis (McDonald’s) Pegmatite

The pegmatite is located on the farm Etusis 75. It is a zoned lithium rich rare metal pegmatite. The pegmatite intruded the metasedimentary rocks of the Karibib Formation. It has been mined for amblygonite, petalite, lepidolite, beryl and bismuth minerals (Diehl, 1992).

Habis Pegmatite

The pegmatite is located 15km south of Karibib on the farm Habis 71. It is described as a lepidolite-beryl rare metal pegmatite (Diehl, 1992).

Daheim Pegmatite

The pegmatite is located on the farm Daheim 106. Petalite mineralisation was found.

Friedrichsfelde Pegmatite

The pegmatite is located on the farm Okakoara 43.

Dobbelsberg Pegmatite

The pegmatite is located on the farm Dobbelsberg 99. Montebrasite- amblygonite mineralisation was found.

Etiro Pegmatite

The pegmatite is located 20km north of Karibib on the farm Etiro 50. The pegmatite forms part of a pegmatite swarm. The pegmatite is 850m long and 4 to 28m wide (Miller, 1969). The pegmatite is a lithium-beryllium rare metal pegmatite. It has well-developed internal zonation. The pegmatite was exploited for feldspar, beryl, mica, columbite-tantalite and bismuth (Diehl, 1992).

South Africa

In the past, pegmatites were considered the only potential source of supply of lithium in South Africa. Spodumene, a member of the pyroxene–group containing 3.73% Li, was considered the only potentially exploitable lithium-bearing mineral in South Africa.

In the Northern Cape and Northern Province, spodumene occurs in zoned pegmatites. In southern Kwazulu-Natal and in the south-eastern part of the Vredefort dome, spodumene occurs in un-zoned pegmatites.

Northern Cape Province

The Namaqualand Metamorphic belt hosts various spodumene-bearing pegmatites, which is confined to the narrow east-west trending “pegmatite belt’ approximately 30km wide and 450km long.Lithium Mining Companies Listed in All Countries

Lithium minerals including spodumene, amblygonite, lepidolite, zinnwaldite, petalite and triphylite-lithiophilite, are found in complex beryl-bearing pegmatites, concentrated in the western parts of the belt, north of Steinkopf.

Individual bodies range from over 2km long and 70m wide to small veinlets, and consist of coarse-grained quartz and feldspar with muscovite, tourmaline and garnet. Spodumene has been extracted from pegmatites on the following properties:

Spodumene Kop 1 and 2

Kokerboomrand 1 and 2

Groenhoekies

Norrabees 1 and 2

Noumas

The Noumas Pegmatite was intermittently worked from 1925 to 1962 for:

bismuth minerals, beryl, tantalum-columbite, muscovite, feldspar and spodumene. The 1 km long by 10 to 42 metres wide pegmatite was emplaced disconcordantly into foliated granodiorite. Spodumene crystals up to 1 m in length are characteristic of the 1 to 8 m intermediate zone, and accounts for up to 50% of the mineral assemblage in places.

Smaller deposits are known from the eastern part of the belt near Kenhardt in the Straussheim 1 and 2, and Angelierspan 1 and 2 pegmatites.

Lithium-bearing pegmatites also occur in the Groendoorn River Gorge, but their small size, remoteness and inaccessibility render them uneconomic.

Production of spodumene from the largest known mineralized pegmatite in Namaqualand totalled 1000 t. Grades were calculated at approximately 5 t spodumene per 100 t of pegmatite. (1865 ppm Li)

Kwazulu-Natal Province

Spodumene in significant quantities has recently been identified in a number of leucocratic pegmatoid bodies on the farm The Corner 11328, south of Mzube River.

The mineralized rocks form part of a suite of sub-concordant predominantly aplitic sills, which intruded mafic gneiss of the Mucklebtraes Formation, Margate Terrane.

The entire package lies within a synformally folded klippen structure. The spodumene-bearing sills, which are the most consistently and well mineralized, are called the Highbury Pegmatites. The sills are up to 15m thick and were emplaced at several structural levels along the northern limb of the synform. The white coarse-grained rocks are composed of quartz, albite, microcline and spodumene with traces of white lithium mica, garnet, graphite and rarely beryl. Pale yellowish green to pink spodumene intergrown with quartz, forms irregular to ovoid poikilocrysts up to 40cm across. This texture is characteristic of spodumene that has replaced primary petalite.

Outcrops with more than 35% intergrown quartz have been recorded intermittently over a 1km strike length. The down-dip extent of the mineralized zone cannot be calculated with the present data and drilling is necessary to establish a reliable resource estimate.

The Li–pegmatites are considered to be late-stage differentiates of the characteristically anhydrous garnet leucogranites and charnockites of the Margate Suite, with which they share many geochemical and mineralogical s

Estimates of global lithium uses in 2011

Ceramics and glass (29%)

Batteries (27%)

Lubricating greases (12%)

Continuous casting (5%)

Air treatment (4%)

Polymers (3%)

Primary aluminum production (2%)

Pharmaceuticals (2%)

Other (16%)

Lithium and its compounds have several industrial applications, including heat-resistant glass and ceramics, high strength-to-weight alloys used in aircraft, lithium batteries and lithium-ion batteries. These uses consume more than half of lithium production. In the later years of the 20th century, owing to its high electrochemical potential, lithium became an important component of the electrolyte and of one of the electrodes in batteries. A typical lithium-ion battery can generate approximately 3 volts, compared with 2.1 volts for lead-acid or 1.5 volts for zinc-carbon cells. Because of its low atomic mass, it also has a high charge- and power-to-weight ratio. Lithium batteries are disposable (primary) batteries with lithium or its compounds as an anode. Lithium batteries are not to be confused with lithium-ion batteries, which are high energy-density rechargeable batteries. Other rechargeable batteries include the lithium-ion polymer battery, lithium iron phosphate battery, and the nanowire battery.

Petalite (Li2O.Al2O3.8SiO2)

Source: www.realmagick.com

Lithium News

PRICES

There is no international spot price for lithium. Numerous lithium compounds are sold. The price will depend on the type, purity, particle size, packaging etc. It has been announced that SQM (Chile), the world’s largest supplier of lithium products, will reduce the price of lithium carbonate and lithium hydroxide by 20% at the beginning of 2010. The new prices will be in the range of US$5,000 - 5,400 per tonne (US$2.3-2.4/ per lb). The reason for the decrease in the price is to accelerate the demand recovery and create incentives for researching new uses for lithium (Industrial Minerals, 2009a).

Technical grade carbonate, used for the manufacturing of batteries, cost US$6,613 per tonne in March 2009 (Madison Avenue Research Group, 2009).

The latest Chile monthly export data shows lithium carbonate prices lower by 2.3% for the year 2014 at US$4,600 per tonne.

The price of 99%-pure lithium carbonate imported to China more than doubled in the two months to the end of December 2015, to $13,000 a tonne

List of tech metals stocks with latest financial data

Enirgi Group's New Technology Allows Significant Lithium Extraction

Lithium has all the elements of a very sound investment as it powers future

By Jesse Riseborough (The Independent)

Thursday, July 05, 2012

INVESTORS from JPMorgan Chase to BlackRock are trying to make money from the exploding popularity of iPads and increasing sales of hybrid cars by investing in producers of lithium for batteries.

Prices for the conductive metal, the lightest in the periodic table, have tripled since 2000 in a market now worth $1bn (€794m) a year as uses expand in vehicles, ceramics, electronics and lubricants.

Apple and Toyota, maker of the Prius electric-gasoline car, have few alternatives as they pursue higher performance and mobility, leading Dahlman Rose analysts to forecast lithium demand will double by 2020.

Talison Lithium, whose shares have gained 22pc in the last month, together with Soc. Quimica & Minera de Chile SA, Rockwood Holdings and FMC, account for almost 95pc of world supply.

Rio Tinto Group, the third-biggest mining company, may join the largest suppliers if it goes ahead with a mine in Serbia it says is capable of producing 20pc of global output of the metal.